What is the Registered Disability Savings Plan?

The Registered Disability Savings Plan (RDSP) provides tax-free money for people who have qualified for the Disability Tax Credit. It provides long-term financial security for people with a disability.

Click to see if you qualify for the Disability Tax Credit.

Key benefits of an RDSP

There are many benefits to opening an RDSP including the fact that the money contributed grows tax-free. Also, anyone can contribute to an RDSP with the written consent of the account holder

- Money contributed grows tax free.

- Anyone can contribute to an RDSP with the written consent of the account holder.

- Contributions can be matched, based on family income, with up to $3,500 a year in Canada Disability Savings Grants (CDSG) and up to $1,000 a year in Canada Disability Savings Bonds (CDSB).

- Carry forward on CDSG and CDSB is available back 10 years or to date of diagnosis.

- The total lifetime contribution for each beneficiary is $200,000, with no annual contribution limits.

- If a parent or grandparent passes away and has a financially dependent child or grandchild, they can transfer up to $200,000 of their RRSP/RRIF or RPP to the dependent’s RDSP on a tax-deferred basis.

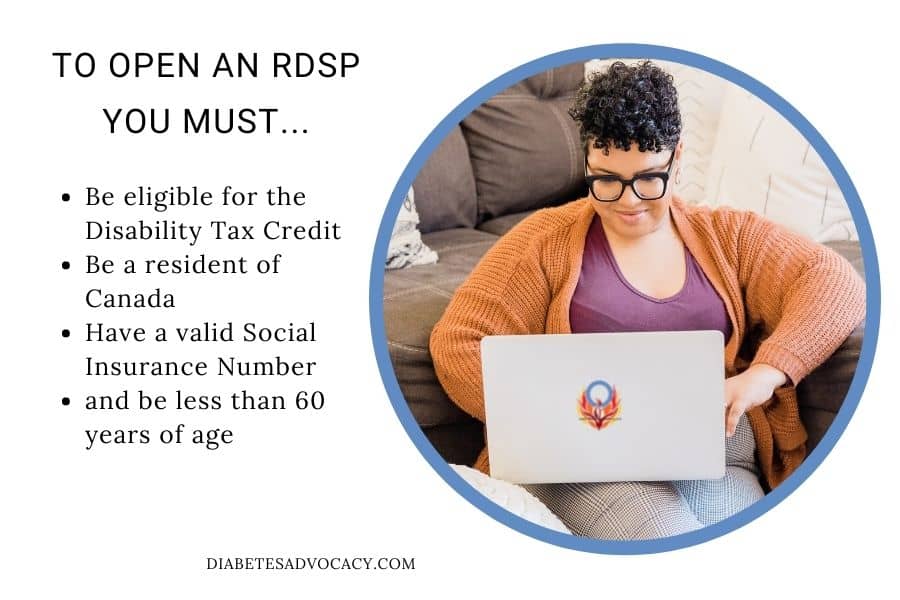

Who is eligible for an RDSP?

To qualify for an RDSP a beneficiary must:

- Be eligible for the Disability Tax Credit

- Be a resident of Canada

- Have a valid Social Insurance Number

- and be less than 60 years of age

The Disability Tax Credit is available to individuals who have mental or physical impairments that markedly restrict their ability to perform one or more of the basic activities of living, such as speaking, hearing or walking. The credit is also available to those who spend more than 14 hours per week on life-sustaining therapy.

The impairment must be expected to last longer than one year. A physician must certify the extent of the disability. There can only be one RDSP account per beneficiary, and only one beneficiary per plan.

Who can be the beneficiary of an RDSP?

To qualify to be the beneficiary of an RDSP, an individual again must:

- Be eligible for the Disability Tax Credit

- Be a resident of Canada

- Have a valid Social Insurance Number (SIN)

- and be less than 60 years of age

How do you maximize your savings?

- Start saving early. Make it automatic by enrolling in a pre-authorized chequing program.

- Take advantage of government grants and bonds and contribute every year to get the maximum annual Canada Disability Savings Grant and Canada Disability Savings Bond.

- Plan withdrawals to avoid federal grant and bond repayments.

What is the Canada Disability Savings Grant (CDSG) and the Canada Disability Savings Bond (CDSB)?

The Canada Disability Savings Grant (CDSG) and the Canada Disability Savings Bond (CDSB) are federal programs that provide payments to RDSPs to encourage long-term savings through an RDSP.

Grants and bonds are available to beneficiaries up until December 31st in the year they reach age 49. Contributions can be matched, based on family income, with up to $70,000 in Canada Disability Savings Grants and up to $20,000 in Canada Disability Savings Bonds. Individual amounts depend on both the beneficiary’s family income and the amount contributed, up to a lifetime maximum CDSG limit of $70,000*

How do you contribute to an RDSP?

Contributions for RDSPs can be made through your local financial institution and invested in a way that best suits you and your goals.

How do I put money into my Registered Disability Savings Plan?

There are five ways to put money into your Registered Disability Savings Plan:

- contributions by the account holder.

- contributions by people the account holder has authorized.

- federal grants and bonds.

- transfers from a qualified or RRSP, RRIF or RPP.

- transfers of the accumulated income from a registered education savings plan on which the beneficiary is on both RESP and RDSP.

When can I begin taking money back out?

You can withdraw the money that you put into an RDSP at any time. Funds must be left in the account for 10 years to receive the full amount of your grant money. (Grant money received in 2013 are not eligible for use until 2023).

Registered Disability Savings Plan with drawls are also known as disability assistance payments. There are two types of payments from an RDSP lifetime disability assistance payments and disability assistance payments.

What good are RDSPs?

Registered Disability Savings Plans are not short term savings vehicles. They are a long term savings for those who cannot afford to save for their own long term medical expenses.

It can also be a safety net in case something happens to the parent. If parents were to pass early, it would give the child a bit of extra financial help towards their care.